Background

Everyone is interested in lowering their taxable income. The desire to personally pay less might be one of the few views consistently shared across all political party lines.

In fact, “tax deduction” might be one of the most commonly used tax-related terms outside financial services circles. The idea that something might lower the amount of income taxed is appealing for obvious reasons.

However, that appeal does not always translate into informed decision-making. For many people, deciding whether they itemize or take the standard deduction can be a point of pride.

This might be less common since the Tax Cuts and Jobs Act drastically increased the standard deduction for all filer types.

Regardless, “Can I deduct this on my tax return?” still comes up regularly.

There are many rules and limitations to a taxpayer’s annual tax filing—as well as when considering retirement tax planning. These should be considered before deciding how to utilize opportunities around itemizing deductions on Schedule A of form 1040.

This article focuses on common misconceptions financial advisors and tax preparers come across when working with their clients on taxes. As you work with yours, this will show you pitfalls to look out for.

Additionally, the article provides suggestions for addressing these topics with your client. Help them make sure they aren’t leaving the IRS a tip.

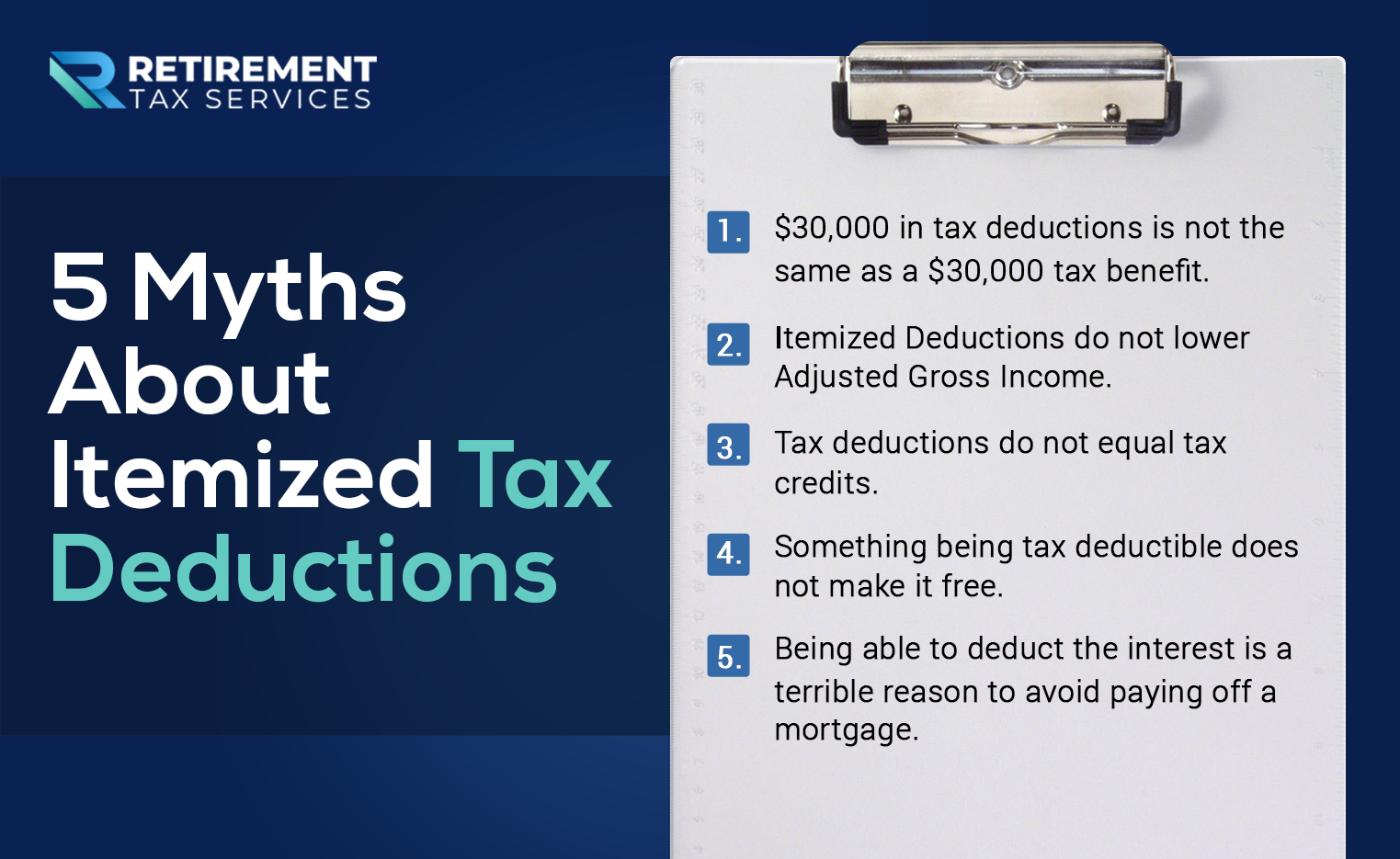

5 Myths About Itemized Tax Deductions

1. $30,000 in tax deductions is not the same as a $30,000 tax benefit.

It’s essential to remember that everyone can take the standard deduction. So, a taxpayer is only really getting a benefit for the deductions above and beyond the standard deduction.

Let’s say a married couple is filing jointly. In 2021, if they had $30,000 in itemized deductions, they would only get a benefit from $4,900 of that. The standard deduction is $25,100 for those who are married but filing jointly.

The benefit is that taxable income is reduced, so you would take the $4,900. Next, you multiply by their marginal tax rate to find how much the deductions impacted the amount of tax owed.

This shouldn’t discourage charitably-inclined taxpayers from giving to qualified charities. However, understanding this context can help with planning around larger gifts. It may help clear up confusion for clients, too.

2. Itemized Deductions do not lower Adjusted Gross Income.

Tax law is filled with rules, limitations and phaseouts based on Adjusted Gross Income (AGI) and Modified Adjusted Gross Income (MAGI). For 2020, that was Line 11 of Form 1040.

The most recent round of COVID-19 stimulus checks is included in the list of tax rules tied to AGI for 2021. If you have a client who is worried about getting phased out due to income, increasing taxable deductions will not help.

Let’s talk retirement tax planning: Limitations on tax advantaged retirement accounts are also linked to AGI (IRS Pub. 590-A).

When financial professionals talk about “above the line” deductions, AGI is the line they are referring to. There are ways to reduce AGI through above-the-line deductions (even if you don’t itemize), but they are not through Schedule A.

Here is a great article from Kiplinger outlining some of the ways this can be done.

More Taxing Myths

3. Tax deductions do not equal tax credits.

Deducting $1 of an expense isn’t the same as $1 less of tax owed.

Tax deductions reduce the total amount your tax rate is applied to. Meanwhile, tax credits reduce the amount of tax you owe.

This means if you owe $10,000 in taxes, a tax credit of $1,000 will result in you owing $9,000, while a tax deduction of $1,000 will only reduce your total tax bill by $220 (assuming you are in the 22% tax bracket).

4. Something being tax deductible does not make it free.

This myth comes up more with small business owners. Regardless, the misconception is prevalent for taxpayers of all kinds (see myth #5 below).

The fact that people often refer to deductions as tax “write-offs” might add to the confusion. At the end of the day though, you still spend money to get the tax benefit.

For every dollar someone in the 22% tax bracket deducts, they save $0.22 in taxes. While that is better than not getting tax savings, it is far from free.

5. Being able to deduct the interest is a terrible reason to avoid paying off a mortgage.

I still hear this one come up: “If I pay off my mortgage, my taxable income will be higher.”

If the client is actually itemizing their deductions, this is a true statement. At the same time, it misses the point: Not paying an expense is universally better than getting a tax deduction from it.

Money is emotional (and this myth is a commonly-held belief) so you need to be tactful. Regardless, the short version is, “Why would it make sense to spend a dollar to save twenty two cents?”

Getting Proactive Pays

There are other ways to add value to your clients regarding tax deductions. Educating them on common misunderstandings is only the beginning.

Take a proactive, long-term approach to retirement tax planning with them. Know what their goals are and what is going on in their lives.

Once you do, there are 2 ways, in particular that are worth exploring. The first is to recommend grouping deductions in specific years instead of evenly over time.

To do this effectively, you have to really know your clients’ goals and intentions. For easy math, let’s say your client would like to give $10,000 to charity every year.

This is well below the current standard deduction. It won’t result in any tax benefit if they make these contributions evenly each year.

However, if they made a $40,000 contribution every 4 years, they would still get the standard deduction in the other 3 years. They would also get an additional $14,900 reduction in taxable income for year 4 (assuming married filing jointly, total deduction of $40,000 less the standard deduction of $25,100).

Once again, make sure you really understand your clients’ goals before going down this road. Their favorite charity could be need of ongoing support operationally more than sporadic large contributions.

Your first goal as the advisor should be helping them accomplish their goals. Learn their “why” for giving—and only then help them accomplish those goals in the most advantageous way possible.

Taking this approach; grouping deductions also provides flexibility when unexpected events occur. For example, another potentially large source for itemizing deductions can be medical bills.

Of course, your clients would rather not have to deal with this situation. Regardless, if they have a year with large medical expenses, adjust the timing of large charitable contributions to that same year. This will further increase their benefit over the standard deduction.

The second strategy to consider is to combine itemized deductions with Roth Conversions (or any other retirement tax planning events generating large amounts of income within a single year).

While itemized deductions do not impact AGI, they do lower taxable income. That is what determines which tax brackets a taxpayer is filling up.

Strategically group itemized deductions, such as charitable giving, in years where you are also recommending strategies that increase taxable income. This will increase the amount of Roth Conversion you can do in a year without going into a new tax bracket.

The same logic applies to years where you are recommending capital gains harvesting.

Take Action

Here is what every great advisor should be doing related to this topic:

- Get tax returns for every client every year. This is the best way to identify retirement tax planning opportunities and learn how charitably inclined your client is. You might find opportunities for recommending a different approach to deductions, as well.

- Provide tax education as a recurring value-add for your clients. If you think this should be the client’s tax preparer’s responsibility, remember: You should take ownership of everything you do. If you want to add value to a client, don’t ever wait for someone to take care of them for you. Partner with a CPA to provide the education. This requires getting proactive beforehand, but it is worth it. Keep in mind that tax preparers tend to be compliance-focused. As a result, most are not as forward-looking as you can be.

- Perform lifetime tax projections for your clients. This provides context for recommending retirement tax planning opportunities, including how to maximize itemized deductions.

Great advisors provide value in all aspects of their clients’ financial lives. CPAs do not have exclusive rights on all things tax-related. In fact, many of them will thank you for taking these steps with your shared clients.

Even if you find yourself in a situation that is beyond your expertise, you can still serve your client and provide value through partnering with them.

Work with the tax experts. Don’t just sit back and say, “Sorry, I don’t give tax advice.”

Good luck out there and remember to tip your server, not the IRS.